Unlocking the Secrets of 831(b): Exploring its Benefits and Strategies

Captive insurance has gained attention in recent years as businesses look for innovative ways to manage risk and potentially lower their tax burden. One such option is the Internal Revenue Code Section 831(b), commonly known as 831(b) or microcaptive. This tax code provision allows small and mid-sized businesses to form their own captive insurance companies, providing them with greater control over their insurance coverage and potential tax advantages.

At first glance, the 831(b) tax code might seem like a complex puzzle. However, by unlocking its secrets and understanding its benefits and strategies, businesses can harness the power of captive insurance to their advantage. In this article, we will dive deep into the world of 831(b), exploring how it works, its potential benefits, and strategies for effectively utilizing it. Whether you are a business owner seeking to manage risk or a financial professional looking to provide valuable insights to clients, this article will equip you with the knowledge needed to navigate the intricacies of 831(b) and make informed decisions. So, let’s begin this journey of exploration and discovery to uncover the hidden potential of 831(b)!

Benefits of 831(b)

-

Tax Advantages: One of the key benefits of utilizing the 831(b) tax code is the potential for significant tax advantages. This provision allows small insurance companies, also known as microcaptives, to be taxed only on their investment income, while the premiums received from policyholders are typically tax-exempt. By taking advantage of this tax structure, businesses may be able to reduce their overall tax liability and retain more of their profits within the captive insurance company.

-

Risk Management: Another advantage of opting for an 831(b) captive insurance arrangement is the increased control and flexibility it provides in managing risks. By establishing their own captive insurance company, businesses can tailor insurance coverage to their specific needs and risks, rather than relying solely on traditional insurance policies. This can result in enhanced coverage, reduced costs, and greater control over the claims process.

-

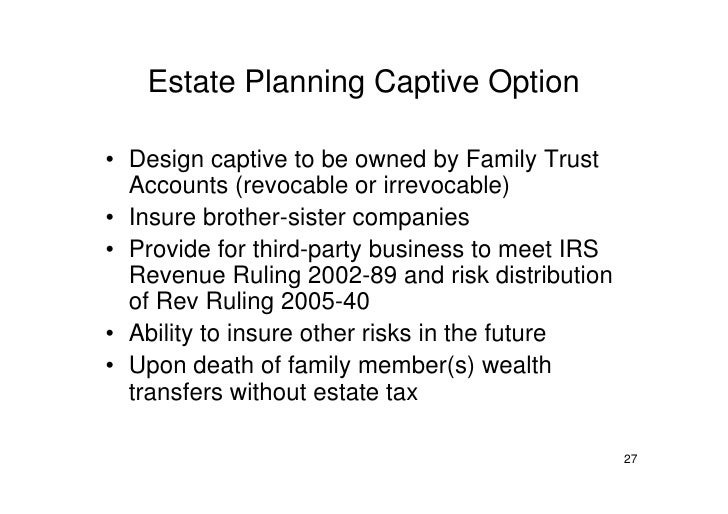

Wealth Transfer: The 831(b) tax code also presents opportunities for wealth transfer and estate planning. Business owners can strategically structure their captive insurance company to facilitate the transfer of wealth to future generations by utilizing strategies such as gifting shares or establishing trusts. This allows for the preservation of family wealth and the potential for significant tax savings in the long run.

Remember, the information provided here is a condensed summary of the benefits associated with the 831(b) tax code. As always, it is important to consult with a qualified tax professional or insurance advisor to fully understand the implications and suitability of this arrangement for your specific business needs.

Strategies for Utilizing 831(b)

In order to effectively utilize the benefits of the 831(b) tax code provision for captive insurance purposes, there are several strategic approaches that can be considered.

1. Risk Mitigation: One key strategy is to use an 831(b) captive insurance arrangement to mitigate risks that may not be adequately covered by traditional insurance policies. By forming a captive insurance company under section 831(b), businesses can tailor coverage to their specific needs, ensuring they are protected against unique risks that may be overlooked by commercial insurers.

2. Tax Advantage Optimization: Another important strategy involves optimizing the tax advantages provided by the 831(b) tax code provision. As a small and micro-insurance company, an 831(b) captive can benefit from specific tax exemptions and reduced tax rates. It is essential to carefully structure and manage the captive insurance company to maximize the tax benefits available under this provision.

3. Wealth Preservation: A third strategy for utilizing 831(b) involves wealth preservation. By establishing a captive insurance company, high-net-worth individuals and families can protect their assets and wealth through risk management strategies while simultaneously enjoying certain tax benefits. This approach offers a more comprehensive and personalized solution for safeguarding wealth and managing potential liabilities.

Each of these strategies allows businesses and individuals to capitalize on the opportunities presented by the 831(b) tax code provision. By considering these approaches and working closely with insurance and tax professionals, one can unlock the full potential of captive insurance arrangements under the 831(b) tax code.

Understanding IRS 831(b) Tax Code

The IRS 831(b) tax code is a provision that allows small insurance companies, also known as microcaptives or captive insurance companies, to receive certain tax benefits. Under this code, eligible companies with premiums not exceeding $2.4 million annually can elect to be taxed only on their investment income and not on their insurance underwriting income.

To qualify for the benefits of the 831(b) tax code, the insurance company must meet certain requirements set by the IRS. These requirements include conducting legitimate insurance operations, having sufficient risk distribution, and demonstrating adequate capitalization.

One of the key advantages of utilizing the 831(b) tax code is the potential tax savings. By electing to be taxed only on their investment income, small insurance companies can potentially reduce their overall tax liability. This can provide them with more financial resources to reinvest in their businesses, expand their services, or improve their financial position.

It is important to note that while the 831(b) tax code can offer valuable tax benefits, its usage has come under increased scrutiny by the IRS. The IRS has identified certain abusive practices in the microcaptives industry and is actively taking steps to address these issues. Therefore, companies considering the utilization of the 831(b) tax code should ensure compliance with the IRS guidelines and seek professional guidance to ensure proper implementation.