Unraveling the Power of Microcaptives: A Deep Dive into the Future of Risk Management

As businesses navigate the ever-changing landscape of risk management, an innovative solution has emerged—the microcaptive. This fascinating concept, rooted in the world of captive insurance, holds the promise of empowering organizations to seize control over their own risk protection. You may have come across the term "831b" or heard murmurs about the IRS 831(b) tax code in relation to microcaptives. In this article, we will take a deep dive into the realm of microcaptives, exploring their potential, benefits, and the future they hold within the realm of risk management.

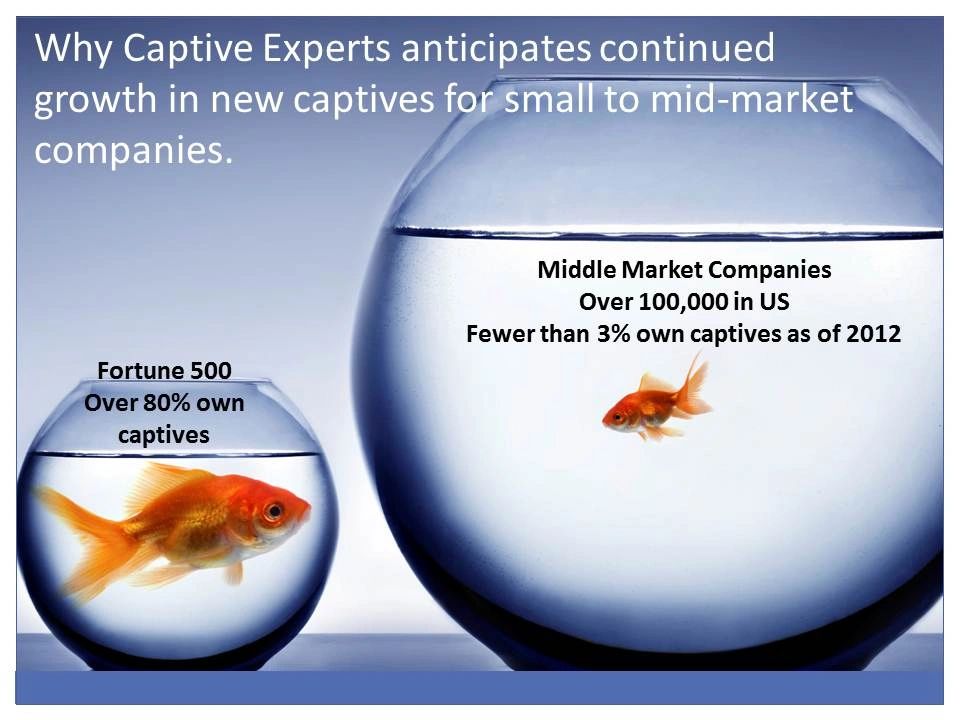

At its core, a microcaptive is a form of captive insurance company, designed to provide coverage for the risks faced by its parent organization. What sets microcaptives apart is their versatility and accessibility. By leveraging the regulatory framework outlined in the IRS 831(b) tax code, small and medium-sized enterprises (SMEs) can establish their own captive insurance, previously considered a luxury only available to larger corporations. This opens up a world of possibilities, as SMEs can now tailor insurance policies directly to their specific needs, effectively managing risks that a traditional insurance market may not adequately address.

Captive insurance, in general, allows organizations to retain control over their risk, offering a layer of protection that complements traditional insurance programs. However, traditional captives often come with high financial thresholds and complex regulatory requirements, making them unattainable for many businesses. Microcaptives, on the other hand, were introduced to bridge this gap, offering a more accessible and cost-effective approach to captive insurance. By harnessing the power of microcaptives, organizations can take advantage of the numerous benefits that come with greater control and customization over their risk mitigation strategies.

In the following sections, we will explore the intricacies of microcaptives, shedding light on how they can revolutionize the risk management landscape for organizations of all sizes. Join us as we unravel the power of microcaptives and delve into their potential impact on the future of risk management.

Understanding Microcaptives

Microcaptives, also known as 831(b) captives, are a particular type of captive insurance company that can offer significant advantages for risk management and tax planning purposes. These entities are formed under Section 831(b) of the Internal Revenue Code, which provides a unique tax treatment for qualifying captive insurance companies. The primary goal of a microcaptive is to provide insurance coverage to its parent company or affiliated businesses, effectively assuming the risks associated with their operations.

The IRS 831(b) tax code is at the core of microcaptives’ appeal. Under this provision, insurance premiums received by a qualifying microcaptive are taxed at a significantly lower rate compared to traditional insurance arrangements. The reduced tax liability can result in substantial savings for businesses that opt for this form of risk management. By forming a microcaptive, companies can achieve greater control over their insurance coverage while potentially benefiting from favorable tax treatment.

To qualify as a microcaptive, certain criteria must be met. The captive must operate as a legitimate insurance company, providing real risk coverage to its insureds. It should also demonstrate sufficient risk distribution, which means that the premiums received are proportionate to the risks involved. Additionally, an 831(b) captive must have a certain level of diversification in terms of its pool of insureds to ensure it is not just acting as a vehicle for tax avoidance.

Microcaptives have gained attention in recent years as businesses look for ways to enhance their risk management strategies and optimize their tax planning. These entities offer flexibility and control over insurance coverage, along with potential tax advantages. However, it is important to carefully navigate the legal and regulatory landscape as microcaptives have faced scrutiny from the IRS, particularly in relation to compliance with the qualifying criteria. It is crucial for businesses considering a microcaptive to consult with qualified professionals to ensure compliance with all applicable regulations while maximizing the benefits of this risk management tool.

Remember, always seek professional advice and conduct thorough research before making any decisions regarding microcaptives or any other financial matters.

The Benefits of Captive Insurance

Captive insurance, also known as microcaptive insurance under the IRS 831(b) tax code, offers several advantages for businesses looking to manage and mitigate their risks. By setting up their own insurance company, organizations can tailor their coverage to suit their unique needs, resulting in greater control and flexibility over their risk management strategies.

-

Tailored Risk Management:

By establishing a captive insurance company, businesses can customize their insurance solutions to address specific risks. This allows them to design policies that align precisely with the nature of their operations and the unique challenges they face. With the ability to target and adapt coverage as needed, organizations can significantly improve their risk management efforts. -

Cost Savings:

Captive insurance offers the potential for significant cost savings compared to traditional insurance arrangements. By retaining a portion of the risk themselves, businesses can reduce their reliance on external insurers and avoid paying sizable premiums. Furthermore, captives enable organizations to access more favorable reinsurance terms, resulting in further cost reductions and potentially higher returns on investment. -

Enhanced Control:

Captive Insurance

One of the most significant benefits of captive insurance is the increased control it provides to organizations. By managing their own insurance company, businesses have an active role in decision-making processes regarding coverage, policy terms, claims, and underwriting guidelines. This level of control allows for greater responsiveness to changing risks and market dynamics, giving organizations a competitive edge in managing their exposures.

In conclusion, captive insurance offers numerous benefits, including tailored risk management, cost savings, and enhanced control. As businesses continue to face evolving risks, exploring microcaptives and the potential of the IRS 831(b) tax code can provide a strategic advantage in navigating the future of risk management.

Navigating the IRS 831(b) Tax Code

The IRS 831(b) tax code is a crucial element to understanding and utilizing microcaptives effectively. Under this specific section of the tax code, smaller insurance companies, known as microcaptives, can elect to be taxed only on their investment income. This provides them with significant tax advantages and the opportunity to accumulate funds for future liabilities.

Operating as a captive insurance company enables businesses to form their own insurance subsidiaries and manage their risks more strategically. By doing so, they gain more control over their insurance programs and can tailor coverage to their specific needs. The IRS 831(b) tax code provides an added incentive for businesses to establish microcaptives, allowing them to enjoy tax benefits while strengthening their risk management practices.

Microcaptives that comply with the IRS 831(b) tax code regulations are eligible for specific tax advantages. One advantage is the ability to deduct premiums paid to the captive as ordinary and necessary business expenses. This deduction can help reduce the overall tax burden for the parent company while effectively transferring risk to the captive.

It’s important to note that the IRS has implemented stringent regulations surrounding the use of microcaptives to prevent abuse and ensure that they are established for genuine risk management purposes. Due to the potential for misuse, it is essential for businesses to navigate the IRS 831(b) tax code carefully. Compliance with the regulations will not only safeguard businesses from potential penalties but also enable them to leverage the benefits offered by microcaptives effectively.